Financial Independence for Latinas: 5 Steps to Mastering Your Money and Budget.

The hard truth of 2026 is that the system wasn’t designed for us to win. Many women reaching retirement age today are slipping into poverty because they were taught to save, but never taught to invest. Including many señoras in my family and friends who have to survive on only social security as the rise of inflation eats up money, power, and, jobs are not as easily available. Relying on a spouse or partner is no longer a viable plan; it puts your future in a vulnerable position.

In this post, we’ll explain why latina’s financial retirement planning is a matter of survival, especially for Latinas who face the steepest wage gaps. We will cover the steps to calculate your Financial Independence Retire Early number, how to move from an “Ahorros” mindset to an “Inversionista” mindset, and provide 5 actionable suggestions for Latinas ready to build generational wealth.

No One is Coming to Save Us

As the eldest daughter in a Latino household, you’ve likely spent your life navigating two cultures, two languages, and now, a complex digital economy. Our parents gave us the best advice they had, “ahorra tu dinero” but in 2026, you cannot save your way to being a millionaire. Inflation and the rising cost of living have made the old rules obsolete.

Too many of us have become our parents’ only retirement plan. To break this cycle, we must stop being just “savers” and start being “investors.” We aren’t just doing this for ourselves; we are doing it so the next generation doesn’t have to carry the same weight we do.

The Math: Saving vs. Investing

If you save $500 a month in a standard bank account, it will take you 166 years to become a millionaire. If you invest that same $500 in an index fund with an average 7-10% return, you could reach that goal in 40 years.

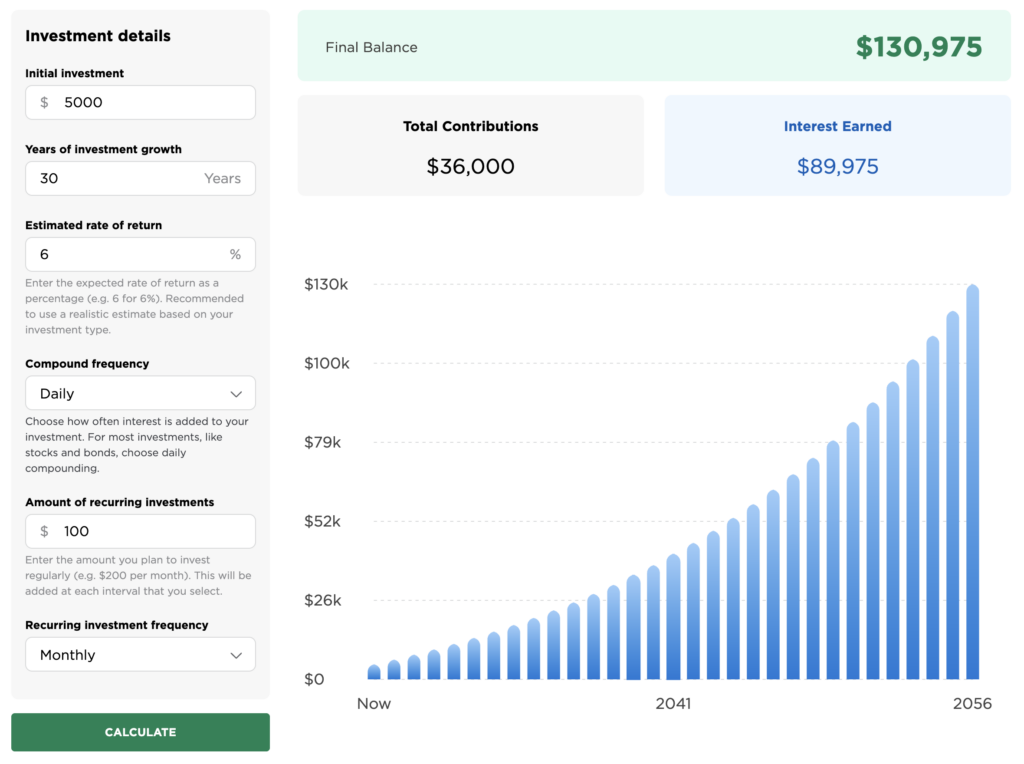

Compound interest does the heavy lifting, so you don’t have to work until you’re 90. Even starting with $50 per paycheck makes a difference. Below is an example of my favorite Investment Calculator by Nerd Wallet. Let’s say you have been investing for the last year, and you started with 5,000 and invested $100 every month. $100 after 30 years, an estimated return rate of 6%, your total contributions are 36,000, the interest earned is 89,975, for a total balance of $130,975.

What is Financial Independence, and Why Does it Matter?

Financial Independence (FI) isn’t about being rich; it’s about having enough wealth that work becomes optional. For a long time, the finance world has used jargon to confuse us. They want us to believe it’s too complicated, so we pay high fees to advisors.

I realized this wasn’t true after reading Girls That Invest by Simran Kaur. As the granddaughter of humble farmers, I learned that I belong in the market; we are all in the market. Whether it is Index Funds, ETFs, or Stocks, the goal is the same: putting your money to work and having it compound over time will set us up for a better future. With the uncertainty of Social Security in 2026, we cannot rely on the government. We must rely on our portfolios.

Stocks: The “Single Ingredient”

When you buy a stock, you are buying a tiny piece of one specific company (like American Express, Coca-Cola, or Costco).

How it works: If that company does well, your stock value goes up. If that specific company fails, you could lose everything you put into it.

Vibe: High risk, high potential reward. I wouldn’t put all your eggs in one basket. Even when I worked in Big Tech, I would never concentrate all of my wealth in one company. I would diversify my investment.

ETFs (Exchange-Traded Funds): The “Basket”

An ETF is a “basket” of many different stocks bundled together. When you buy one share of an ETF, you are actually buying a tiny slice of hundreds of different companies at once.

How it works: You buy and sell them on the stock market all day long, just like a regular stock.

Vibe: Medium risk because you are diversified (if one company in the basket fails, the others can balance it out). It’s like buying a pre-made fruit salad.

Index Funds: The “Recipe”

An Index Fund is a type of fund (it can be an ETF or a Mutual Fund) that is designed to mimic a specific list. For example, an S&P 500 Index Fund simply buys the 500 largest companies in the US.

In 2007, Buffett bet $1 million that a basic S&P 500 index fund would outperform a hand-picked group of high-priced hedge funds over a 10-year period The Contender: Ted Seides of Protégé Partners accepted the bet. The Index Fund: Returned about 7.1% annually. The Hedge Funds: Returned an average of only 2.2% annually. Essentially, the “boring” index fund made four times more money than the expert-managed funds over that decade.

How it works: There is no “expert” picking stocks; a computer just follows the list (the “index”). Because no expensive managers are involved, the fees are usually much lower.

Vibe: Slow and steady. You aren’t trying to “beat” the market; you are just trying to be the market.

How I Built a Plan Toward Financial Independence as a Latina

Phase 1: Creating a Budget

It can feel restrictive at first. I didn’t want to create a budget, but then I realized that it helped me give every dollar I make a job. Instead, treat your budget as a “permission slip” to spend on what matters while ensuring your future self is cared for.

- The 50/30/20 Rule:

- 50% Needs: Rent, groceries, and minimum debt payments.

- 30% Wants: This includes priorities like travel to see family or community celebrations.

- 20% Savings & Extra Debt Repayment: This is your engine for financial independence.

- The “Three Bucket” System: Divide your income into Expenses (bills), Goals (debt/savings), and Fun (lifestyle). Automate the “Goals” bucket so you don’t have to choose between family obligations and your debt payoff every month.

Phase 2: Calculate Your Net Worth

Your Net Worth is an overhead shot of your financial power at this exact moment. To master your money, you have to know your numbers. Think of this as the “Financial Health Check-In” for your household. Before you can build wealth, you have to see exactly where you are standing. This can feel scary, but it’s better to know exactly where you are than guess and waste your time on the wrong goal.

It isn’t just about how much is in your accounts; it’s the difference between what you own and what you owe.

The Formula:

Assets – Liabilities = Net Worth

- Assets (What you own): Cash in the bank or brokerage, the value of your car, your 401k/Roth IRA balance, and any real estate you own.

- Liabilities (What you owe): Credit card balances, student loans, car loans, and your mortgage.

Why it matters: In 2026, many of us feel “broke” because our bank account is low, but your Net Worth might actually be growing because we’re paying down debt or your 401k is rising. Tracking this helps you stay motivated when the daily grind feels tough.

Phase 3: Determine Your FIRE Number

The “FIRE Number” is the amount of money you need invested so that you never have to work again. This is the goal for true financial independence.

The “Rule of 25”:

To find your number, take your annual survival expenses (the bare minimum you need to live for one year) and multiply it by 25.

Annual Expenses x 25 = Your FIRE Number

Example:

If you need $40,000 a year to cover rent, groceries, and bills:

- $40,000 x 25 =$ $1,000,000

Phase 4: The 4% Rule (How it works)

Once you hit your FIRE Number, you can live off the 4% Rule. This is a math-based strategy that suggests if you withdraw 4% of your total investments each year, your portfolio will likely never run out of money because it continues to grow in the market.

- Your $1M Portfolio generates roughly $70,000–$100,000 in growth each year.

- You take out $40,000 (4%) to live on.

- The rest stays in the account to keep growing and beating inflation.

Comparison Table: What’s your goal?

Monthly Expenses | Annual Expenses | Your FIRE Number (x25) |

$3,000 | $36,000 | $900,000 |

$4,000 | $48,000 | $1,200,000 |

$5,000 | $60,000 | $1,500,000 |

Pro-Tip for 2026: For Latinas in the “sandwich generation,” make sure your annual expenses include a buffer for family emergencies or medical care for parents. We don’t just plan for ourselves; we plan for our community.

Phase 5: The Tax Advantage Accounts (401k, 403b, 457b)

These are accounts set up by your job. The money is taken directly out of your paycheck before you even see it—which makes “paying your future self” automatic.

- 401(k): For people at private companies (Costco, Google, local businesses).

- 403(b): For people at non-profits, schools, or hospitals (teachers, nurses).

- 457(b): For state and local government employees (firefighters, police).

The Magic Word: “The Match” Many employers offer a match. If you put in 5%, they might give you an extra 5% for free.

Action Step: Always contribute at least enough to get the full match. If you don’t, you are literally leaving a “free raise” on the table.

The Individual Account (Roth IRA)

While a 401k is tied to your job, a Roth IRA is an account you own and control. You open this yourself at a brokerage like Schwab or Fidelity.

- The “Pay Taxes Now” Benefit: You put in money that has already been taxed (from your bank account).

- The Payoff: Because you paid taxes today, every dollar you earn in that account is 100% tax-free when you retire. If you invest $5,000 and it grows to $50,000, you keep the whole $50,000.

- Flexibility: Unlike a 401k, you can withdraw your contributions (the original money you put in) at any time without penalty if there’s an emergency.

The Health Savings Account “Triple Tax Advantage”

The HSA is even more tax-efficient than a 401k or a Roth IRA because it combines the best of both:

Tax-Free In: Contributions are 100% tax-deductible (like a Traditional 401k), lowering your taxable income today.

Tax-Free Growth: Your investments inside the account grow without the IRS taking a cut.

Tax-Free Out: Withdrawals are 100% tax-free (like a Roth IRA) as long as they are used for qualified medical expenses.

Most people use an HSA like a checking account—put money in, spend it on a doctor’s visit, repeat. However, “power users” treat it as a retirement account:

Invest the funds: You don’t have to keep the money in cash.7 You can invest it in stocks/ETFs just like an IRA.

2026 Contribution Limits

| Account Type | 2026 Contribution Limit | Details |

Health Savings Account (HSA) | $4,400 (Self-Only Coverage) | The family coverage limit is projected to be $8,750. An additional catch-up contribution of $1,000 applies for those age 55 and older. |

Roth IRA (Base Limit) | $7,500 | This is the base limit for individuals under age 50. The total limit with the projected catch-up contribution for those age 50 and older is $8,600 (base limit + $1,100 catch-up). This limit is shared with Traditional IRAs. |

457(b) Deferred Compensation Plan (Employee Deferral) | $24,500 | This is the limit for employee elective deferrals (under age 50). A separate catch-up contribution applies for those age 50 and older. |

401(k) Plan (Employee Deferral) | $24,500 | This is the limit for employee elective deferrals (under age 50). The total limit, including the projected catch-up contribution for those age 50 and older is $32,500 ($24,500 + $8,000 catch-up). |

| SEP IRA (Maximum Annual Addition) | $72,000 | This is for Business owners, and the contribution is limited to the lesser of this amount or 25% of the employee’s compensation. |

Closing

Financial independence is the ultimate form of protest against a system that pays Latinas 57 cents for every dollar a white man earns. It provides the freedom to leave unhealthy jobs, exit bad relationships, and support your community. It took me until I was 36 to take this seriously, but it is never too late to start. Thanks to attending Janesse Torre’s Our Money Our Power Summit in Puerto Rico, I decided I was going to be in charge of my finances. Your future self is counting on you to take the first step today.